Coming Home: Keys to Smart Home Buying

Buying a home is one of life’s most important investments and exciting adventures, but even experienced buyers can find this complex process a bit overwhelming. As your Coldwell Banker Sales Associate, I will guide you every step of the way. In addition to the crucial step of locating and presenting properties that match your search criteria, I will be helping you all along the path between “I want this house!” and “I own this house!”

TOGETHER, WE CAN USE THIS HELPFUL GUIDE FOR:

-

Determining your price range based on your estimated monthly payments

-

Deciding what you want in a home

-

Understanding the asking price

-

Negotiating the offer and contract

-

Getting the mortgage application underway

-

Facilitating the financing process

-

Initiating the property evaluation and inspection process

-

Understanding the title search process

-

Preparing you for the close of escrow and associated costs

DETERMINING YOUR PRICE RANGE…HOW MUCH HOUSE CAN YOU AFFORD?

While lenders use different formulas for arriving at this figure, most prefer that you spend no more than 28% of your gross monthly income on housing costs or PITI (principal, interest, taxes and insurance) and no more than 38% on combined total monthly house and long-term debt payments. However, each person’s financial picture is unique and I ’ll be happy to put you in touch with a lender I trust to evaluate your buying power. To make sure that I’m showing you properties that fit comfortably within your price range, please take a moment to complete this brief Home Affordability Worksheet.*

|

Home Affordability Worksheet

|

Example

|

You

|

|

1. Gross Annual Income (before taxes)

|

$75,000 |

|

|

2. Gross Monthly Income (line 1 divided by 12) |

$6,250 |

|

|

3. Monthly Allowable Housing Expense and Long-term Obligations (line 2 multiplied by .38) |

$2,375 |

|

|

38% of gross monthly income is typically allocated for principal, interest, taxes, insurance (PITI) and monthly long-term obligations. |

||

|

4. Monthly Obligations – ie. credit card payments, car loans, child support, etc. |

$500 |

|

|

5. Monthly Allowable Housing Expense (line 3 minus your monthly obligations on line 4) |

$1,875 |

|

|

The remainder is your allowable PITI payment. The Monthly Allowable Housing Expense on line 5 should not exceed 33% of line 2. If it does, enter the lesser amount of the two on line 3 and continue. |

||

|

6. Monthly Principal and Interest Payment (line 5 multiplied by .80) |

$1,500 |

|

|

80% is the amount of the Monthly Allowable Housing Expense typically allocated to only the principal and interest portion of your mortgage payment, excluding taxes and insurance. |

||

|

7. Estimated Mortgage Amount (line 6 divided by the interest rate factor assigned to your target interest rate on the Interest Rate Factor Chart on the next page and then multiplied by $1,000) |

$214,592 |

|

|

For this example, we used 6.99, the interest rate factor for a 7-1/2% loan amortized over a 30-year term. |

||

|

8. Estimated Affordable Home Price (line 7 divided by .80) |

$268,240 |

|

|

80% is the mortgage loan amount assuming a 20% down payment. Use 90% for a 10% down payment. |

Again, keep in mind that your rate and affordable price will vary depending on the down payment, specific terms of your loan, and other monthly obligations that you have or may incur with the purchases such as homeowners association fees and dues. While these are standard industry guidelines, there are a variety of mortgage products with flexible options to meet your needs.

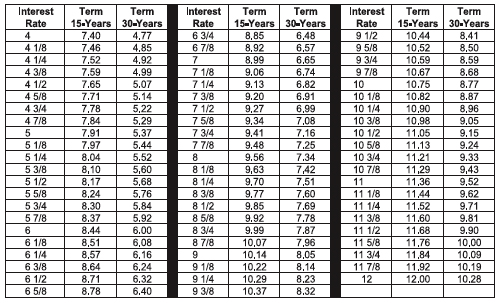

HOW INTEREST RATES AFFECT YOUR MORTGAGE PAYMENT

The chart below will help you calculate your monthly principal and interest payments for both fixed and adjustable rate loans at various interest rates over 15- and 30-year terms.

Start by finding the interest rate. Then go across to the figure under the desired term of the loan. This is the interest rate factor. Multiply this figure by the total loan amount (in thousands) to calculate your principal and interest payment. For example, at 8% interest, the interest factor on a $300,000 30-year loan is 7.34. Multiplying 300 ($300,000 = 300 x 1,000) by the interest factor of 7.34 equals a mortgage payment of $2,202. This would be the principal and interest portion of the mortgage payment only. It does not include property taxes, homeowners insurance, association dues or other charges. A figure that includes only principal and interest is referred to as “PI,” while a figure that includes principal, interest, taxes and insurance is called “PITI.”

FIXED RATE MORTGAGES VS. ADJUSTABLE RATE MORTGAGES (ARM)

The two most common types of mortgages for financing a home are fixed ratemortgages and adjustable rate mortgages (ARM). With a fixed rate mortgage, the interest rate stays the same for the entire term of the loan, usually 15 or 30 years, so the combined principal and interest portion of your payment (PI) does not change. The interest rate on an adjustable rate mortgage is linked to a financial index, so the interest portion of your payment can vary over the life of your loan. Your lender can help you evaluate which type of financing is best for you.

FINDING THE RIGHT HOME

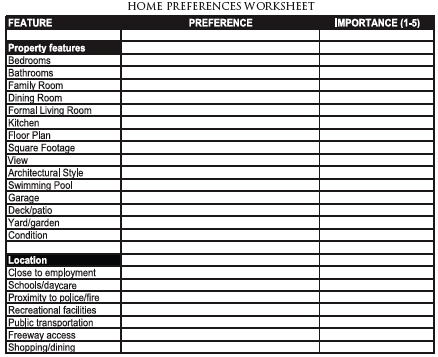

Understanding exactly what you are looking for in your next home will help me create a successful Home Finding Plan for you. Please take a moment to complete this Home Preferences Worksheet.

Indicate how many bedrooms and bathrooms you need and any special features you desire such as a jetted tub or a separate master suite. Consider how important having a family room, bonus/game room, dining room or formal living room is to your lifestyle. Do you long for a kitchen designed for gourmet cooking or will a simple, functional kitchen meet your needs? What architectural and decorative style most appeals to you – single level, two-story or multi-level, traditional or contemporary, bold and modern or warm and rustic? Indicate if having a swimming pool, a view or a big yard is a priority. Determine how location or proximity to certain facilities and amenities will influence your opinion of a property.

Then rate on a scale of 1 to 5 how important all of these factors are to your satisfaction with your next home (1=Not Important at all, 2=Minimal Importance, 3=Somewhat Important, 4=Very Important, 5=I won’t consider any home with/without this!).

Unless you are building your dream home from the ground up, there are often compromises involved in deciding whether or not you will be satisfied with a given property. However, the more I know about your preferences, needs and priorities, the better able I will be to focus our search on properties that most closely match your criteria.

UNDERSTANDING THE ASKING PRICE

Many factors influence the price that a seller expects to get for their home. While only you can decide how much you feel comfortable offering for a property, I can gather critical information for you regarding the factors that impact how much you should consider paying for the home, such as:

-

How long the home has been on the market

-

If the price has been reduced

-

The prices for other comparable homes in the area

-

If there are multiple offers

-

Other items that might be included in the sale – furniture, hot tub, etc.

-

The “list to sale price ratio,” an indication of how competitive the market is for homes in this area

-

Why the seller is selling

-

Whether the seller is offering an assumable loan or financing

GETTING YOUR MORTGAGE APPLICATION STARTED

Being pre-approved by a lender can put you in a much stronger negotiating position, because it shows the seller that you are a committed buyer, financially capable of buying the property and more likely to close on the property. Pre-approval is different from pre-qualification, which is merely an estimate of what you may be able to afford. Pre-approval occurs when the lender has reviewed your credit and believes that you can finance a home up to a specific amount. However, neither pre-approval nor pre-qualification represents or implies a commitment on the part of a lender to actually fund a loan. Here are some of the current documents you’ll need to get started:

INCOME

-

Current pay stubs

-

W-2s or 1099s

-

Tax returns, usually for two years

ASSETS

-

Bank statements

-

Investments/brokerage firm statements

-

Net worth of businesses owned (if applicable)

DEBTS

-

Credit card statements

-

Loan statements

-

Alimony/child support payments (if applicable)

NAVIGATING THE FINANCING PROCESS

The financing process can take anywhere from 10 to 90 days, but typically runs 30 to 45 days. I’ll be involved throughout the process to help it run smoothly. The basic timeline for what will happen along the way is as follows:

-

You submit the completed application and any required supporting documentation to the lender

-

The lender orders an appraisal of the property, a credit report and begins verifying youremployment and assets

-

The lender provides a good faith estimate of closing and related costs, plus initial Truth inLending disclosures

-

The lender evaluates the application and your supporting documents, approves the loan andissues a letter of commitment

-

You sign the closing loan documents and the loan is funded

-

The lender sends its funds to escrow

-

All appropriate documents are recorded at the County Recorder’s Office, the seller is paid andthe title to the home is yours

NEGOTIATING THE OFFER AND CONTRACT

You may make your offer subject to certain terms or contingencies, including securing of financing or perhaps the sale of your current home. You may also make the contract subject to various inspections by both you and professional inspectors. Most contracts include some standard provisions, such as property taxes, insurance costs, utility bills and special assessments that will be prorated between buyer and seller. Others outline what happens if the property is damaged before closing, or if either party fails to go through with the sale. I will review every aspect of your offer and contract with you. Together, we will plan a strategy for getting the most advantageous terms for you, the buyer, at the price you are willing to pay for the property.

INSPECTIONS

Real estate contracts often contain contingency clauses that allow buyers to inspect the property. Certain inspections are required by lenders and others are a matter of observation and what is particular to a region or area. Which party pays for these inspections is negotiable. The two most common types of inspection are:

-

Wood Destroying Pest and Organisms (Termite) Inspection This inspection identifies existing or potential pest, dry rot, fungus and other structure-threatening infestation or conditions. The initial inspection fee covers only those areas which are accessible to the inspector. Inspections of inaccessible areas cost more and are subject to an estimate by the inspector. These inspectors must be licensed and can give estimates to correct noted problems, can make the suggested repairs and/or can certify that the work has been completed.

-

General House Inspection This inspection identifies material defects in the essential components of the property based upon a noninvasive physical inspection. There are no licensing requirements for someone to be a home inspector. These inspectors are not allowed to give estimates to correct noted problems, nor can the inspector perform any of the repairs.

UNDERSTANDING THE TITLE SEARCH PROCESS

A title spells out who has the right of ownership for a property. It is considered “clear” if there are no claims or liens against it. In order to make sure nothing will prevent transfer of the property to you, a title company will conduct a title search and prepare a preliminary report that indicates what recorded matters affect the title to the property and if the title insurance company is willing to insure the title. At the close of escrow, the title company will issue an Owner’s Policy of Title Insurance to protect you against losses that might arise from covered claims on the title.

PREPARING FOR THE CLOSING COSTS

A home purchase is a complex transaction involving many parties and associated fees. In addition to your deposit and down payment, there are a variety of other costs involved in the close of escrow:

-

Loan origination fees, appraisals and reports

-

Surveys and inspections

-

Mortgage insurance

-

Hazard insurance

-

Taxes

-

Assessments

-

Title Insurance, notary and escrow fees

-

Recording fees and stamps

The lender will provide a good faith estimate of these costs prior to the close of escrow, so that you will know in advance what to expect. Some of these costs may be negotiable items with the seller. Naturally, I’ll walk you through each item in your closing to make sure you understand every detail.

GLOSSARY: LEARNING A NEW LANGUAGE

Understanding the terms used throughout a real estate transaction can almost seem like learning a whole new language. We’ve created this handy glossary to help you master the vocabulary of real estate.

Adjustable Rate Mortgage (ARM): A mortgage with an interest rate that changes over time in line with movements in afinancial index. ARMs can also be referred to as AMLs (adjustable mortgage loans) or VRMs (variable rate mortgages).

Adjustment Period: The length of time between interest rate changes on an ARM. For example, a loan with an adjustmentperiod of one year is called a one-year ARM, meaning that the interest rate can change once a year.

Amortization: Repayment of a loan in installments of principal and interest, rather than interest-only payments.

Appraisal: An estimate of the property’s value.

Assessed Value: The value placed on a property for purposes of taxation.

Assumption of Mortgage: A buyer’s agreement to assume the liability under an existing note that is secured by a mortgageor deed of trust. The lender must approve the buyer in order to release the original borrower (typically the seller) from liability.

Balloon Payment: A lump sum principal payment due at the end of some mortgages or other long-term loans.

Buydown: A permanent buydown is pre-paid interest that brings the note rate on the loan down to a lower, permanent rate. A temporary buydown is pre-paid interest that lowers the note rate temporarily on the loan, allowing the buyer to more readily qualify and increase payments as income grows.

Cap: The limit on how much an interest rate or monthly payment can change, either at each adjustment or over the life of a mortgage.

Cash Reserves: The amount of the buyer’s liquid cash remaining after making the down payment and paying all closing costs.

CC&Rs or Covenants, Conditions and Restrictions: A recorded document that controls the use, requirements and restrictions of a property.

Commission: An amount paid by the seller to the listing and selling agent for handling the real estate transaction.

Commitment Period: The period of time during which a loan approval is valid.

Condominium: A form of real estate ownership in which the owner receives exclusive title to a particular unit and shares ownership in certain common areas with other unit owners. The unit itself is generally a separately owned space whose interior surface (walls, floors and ceiling) serve as its boundaries.

Contingency: A condition that must be satisfied before a contract is binding. For example, a sales agreement or offer may be contingent upon the buyer obtaining financing.

Conversion Clause: A provision in some ARMs that enables home buyers to change an ARM to a fixed rate mortgage, usually after the first adjustment period. The new fixed rate is generally set at the prevailing interest rate for fixed rate mortgages. This conversion feature may involve an extra charge.

Cooperative: A form of multiple ownership in which a corporation or business trust entity holds title to a property and grants occupancy rights to shareholders by means of proprietary leases or similar arrangements.

CRB or Certified Residential Broker: To be certified, a broker must be a member of the National Association of Realtors¨, have five years of experience as a licensed broker and have completed required Residential Division courses.

Debt Ratios: The comparison of a buyer’s housing costs to his or her gross or net effective income and the comparison of a buyer’s total long-term debt to his or her gross or net effective income. The first ratio is thehousing ratio and the second is the total debt ratio.

Deed: A document which, when properly executed and delivered, conveys title of real property.

Disclosure: To make known or public. By law, a seller of real property must disclose facts which affect the value or desirability of the property.

Discount Points: A negotiable fee paid to the lender to secure financing to the buyer. Discount points are interest chargespaid up-front to reduce the interest rate on the loan over the life or a portion of the term.

Due-on-Sale Clause: A clause that requires a full payment of a mortgage or deed of trust when the secured property changes ownership.

Earnest Money: The portion of the down payment delivered to the seller or escrow agent by the purchaser with a writtenoffer as evidence of good faith.

Easement: A right to use all or part of the land owned by another for a specific purpose. For example, an easement may entitle the holder to install and maintain sewer or utility lines.

Encumbrance: Anything that affects or limits the ownership of real property, such as mortgages, liens, easements or restrictionsof any kind.

Escrow: A procedure in which a third party acts as a stakeholder for both the buyer and the seller, carrying out both parties’ instructions and assuming responsibility for handling all of the paperwork and distribution of funds. An escrow fee, typically paid by the buyer, is charged by the title company to service the transaction and to escrow money and documents.

Equity: The difference between what is owed and the amount for which the property could be sold.

FHA Loan: A loan insured by the Federal Housing Administration (of the Department of Housing and Urban Development).

Federal Home Loan Mortgage Corporation (FHLMC): Often referred to as “Freddie Mac,” they purchase loans from savings and loan lenders within the Federal Home Loan Bank Board.

Federal National Mortgage Association (FNMA): Popularly known as “Fannie Mae,” they purchase and sell residential mortgages insured by FHA or guaranteed by the VA, as well as conventional home mortgages.

Fee Simple: An estate in which the owner has unrestricted power to dispose of the property as he or she wishes, including leaving by will or inheritance.

Fixed Rate Mortgage: A conventional loan with the same interest rate for the life of the loan.

Fixtures: Personal property that is attached to real property and is legally treated as real property while it is attached – such as light fixtures, window treatments and medicine cabinets.

Fully Indexed Rate: The maximum interest rate on an ARM that can be reached at the first adjustment.

Gift Letter: A letter from a relative stating that an amount will be gifted to the buyer and that said amount is not to be repaid.

Government National Mortgage Association (GNMA): Known as “Ginnie Mae,” a governmental part of the secondary market that deals primarily with recycling VA and FHA mortgages, particularly those that are highly leveraged.

Graduated Payment Mortgage: A residential mortgage with monthly payments that start at a low level and increase at apredetermined rate.

Home Warranty Plan: Protection against failure of mechanical systems within the property and usually includes plumbing,electrical, heating and cooling systems and installed appliances.

Index: A measure of interest rate changes used to determine changes in an ARM’s interest rate over the term of the loan.

Initial Interest Rate: The introductory interest rate on a loan, which signals that there may be rate adjustments later in theloan.

Joint Tenancy: An equal, undivided ownership of property by two or more persons. Upon the death of any owner, the survivors take the decedent’s interest in the property.

Jumbo Loans: Mortgage loans that exceed the loan amounts acceptable for sale in the secondary market. Jumbos are packaged and sold differently to investors and have separate underwriting guidelines.

Lien: A legal hold or claim on a property as security for a debt or charge.

List-to-Sale Ratio: The ratio between the price at what a property is listed and the amount for which it is actually sold.

Loan Commitment: A written promise to make a loan for a specified amount on specified terms.

Loan-to-Value Ratio: The relationship between the amount of the mortgage and the appraised value of the property, typically expressed as a percentage of the appraised value.

Lock-in: The fixing of an interest rate or points at a certain level, usually during the loan application process. It is typically fixed for a specified amount of time, such as 20 to 30 days or some other period of time determined by the lender.

Margin: The number of percentage points the lender adds to the index rate to calculate the ARM interest rate at each adjustment.

Mortgage (Deed of Trust): A legal document that provides security for repayment of a promissory note.

Mortgage Insurance Premium (MIP): The mortgage insurance required on FHA loans for the life of said loan. The MIP is either paid in cash at the time of closing or financed over the course of the loan.

Multiple Listing Service: The pooling in a central bureau of all properties for sale. The listings are held individually by members of a group of real estate brokers, with the agreement that any member of the group may sell the properties and the commission will be divided between the broker that sold the property and the broker who filed the listing.

Negative Amortization: Occurs when monthly payments fail to cover the cost of the interest on a loan. The interest that is not covered is added to the unpaid principal balance, meaning that even after making several payments the borrower could owe more than at the beginning of the loan. Negative amortization may occur when an ARM has a payment cap that results in monthly payments that are not high enough to cover the interest.

Origination Fee: A fee or charge for work involved in evaluating, preparing and submitting a proposed mortgage loan. The fee is limited to 1% for FHA and VA loans.

PITI: The term for a mortgage payment that includes principal (P), interest (I), taxes (T) and insurance (I).

Planned Unit Development (PUD): A zoning designation for property developed at the same or slightly greater overall density than conventional development, often with improvements clustered between open or common areas. Use may be residential, commercial or industrial.

Point: An amount equal to 1% of the principal amount of the investment or note.

Prepayment Penalty or Clause: A fee charged to a borrower who pays a loan in full before the stated due date.

Private Mortgage Insurance (PMI): Insurance written by private companies to protect the lender against loss if the borrower defaults on the mortgage. PMI is often required on mortgage loans in which less than 20% has been put forth for the down payment. Depending on the conditions of the mortgage, the borrower may request cancellation of PMI when equity in the property reaches 20%.

Purchase Agreement: A written document in which the purchaser agrees to buy a certain real estate and the seller agrees to sell under stated terms and conditions. Also called a sales contract, earnest money contract, or agreement for sale.

Rate Gap: The difference between the current rate and the rate to which it could adjust on an ARM.

Realtor: A real estate broker or sales associate active in a local real estate board affiliated with the National Association ofRealtors.

Recording Fee: Charged by the County Clerk to record documents in the public records.

Regulation Z: The set of rules governing consumer lending issued by the Federal Reserve Board of Governors in accordance with the Consumer Protection Act.

Tenancy in Common: A type of joint ownership of property by two or more persons with no right of survivorship.

Title: The rights of ownership recognized and protected by law. It is a combination of all elements that constitute the highest legal right to own, possess, use, control, enjoy, transfer and dispose of real estate.

Title Insurance Policy: This policy protects the purchaser, mortgage or other party against defects and losses associated with the title.

Townhouse: Architectural term describing a two or more story unit with no units above or below, but with one or more shared walls. Ownership may be in the form of condominium, planned unit development or stock cooperative.

VA Loan: A loan made by a private lender that is partially guaranteed by the Veterans Administration.

Wood Destroying Pest and Organisms Inspection: An inspection identifying existing or potential pest, dry rot, fungus and other structure-threatening infestation or conditions. Sometimes referred to as “termite inspection.”

Zoning: Laws passed by local governments regulating the size, type, structure, nature and use of land or buildings